Over the last decade, there has been a growing global trend in digital technology products and services, especially in the financial sector. In Nigeria, we’ve seen the introduction of these digital financial services and products such as agent banking, Points-of-Sales (POS), mobile banking, etc. These are supposedly designed to increase economic power and help people make smarter financial decisions. Following this trend, financial inclusion has become a global conversation, leading to the development of the National Financial Inclusion Strategy (NFIS) in Nigeria.

The World Bank defines financial inclusion as a situation in which individuals and their businesses have access to affordable financial products and services that meets their needs and is delivered responsibly and sustainably. These financial products and services include credit, payments, savings and insurance. However, considerable progress has been made globally on financial inclusion, from 49% unbanked adults in 2011 to 31% in 2017. However, when disaggregated, this data presents a gap along gender lines. A good example is the 2017 Global Findex data that reported 72% of men having access to financial accounts while 65% of women had no such financial access.

This gender gap in financial inclusion is particularly challenging because there is incontrovertible evidence that increasing women’s financial access has immense economic and social advantages, as seen in Kenya, South Africa, Tanzania, and Uganda. However, women must first have the awareness and access to financial products like a bank account before accessing credit and other financial products and services.

Financial Inclusion In Nigeria

Like other countries, Nigeria has a financial inclusion strategy. The NFIS was first adopted in 2012 by the CBN to increase access and usage of financial services by 2020. This strategy sought to reduce the number of financially excluded adult Nigerians from 46.3% in 2010 to 20% by 2020 and increase the number of Nigerians included in the formal sector from 36.3% in 2010 to 70% in 2020.

In 2018, the strategy was revised based on the declining adoption of agent banking owing to a lack of understanding of the system and its benefits to stakeholders. A decline in Points-of-Sales (POS) adoption due to technological advancements proved that POS is not the most efficient mode of distributing financial services. The non-adoption of financial products and services is due to traditional and religious factors.

It is impossible to not view financial inclusion in Nigeria through a gendered lens because the level of income, education, and trust in Financial Service Providers (FSPs), the three key drivers of financial inclusion, are gendered. According to EFINA’s 2019 assessment of women’s financial inclusion, about 36% of women are financially excluded as opposed to 24% of men. This figure is now potentially higher due to the COVID-19 pandemic that affected many sectors, especially hospitality & tourism, which record over 54% employment for women. The pandemic has also caused a delay in implementing some financial inclusion strategies, such as the recapitalisation of microfinance banks and insurance companies.

Financial inclusion strategies, including products and services, are currently built around formal tools, but realistically, most women tilt towards informal means for their finances; to earn a living and save if possible, compared to men. This partly explains why the financial inclusion of men keeps increasing, leading to a decline in that of women. Without addressing gender inequality from its root, Nigeria may never achieve its NFIS, and the financial inclusion gap will continue to widen across gender lines.

Why the Gender Equality Gap in Nigeria

As mentioned, there are three key drivers of financial inclusion; level of education, income level, and trust in FSPs that are interwoven, where one impedes the other. Therefore, closing the gender gap in these drivers is necessary for financial inclusion. This gap is culturally motivated. Hence, the conversation about closing the financial inclusion gender gap is broad.

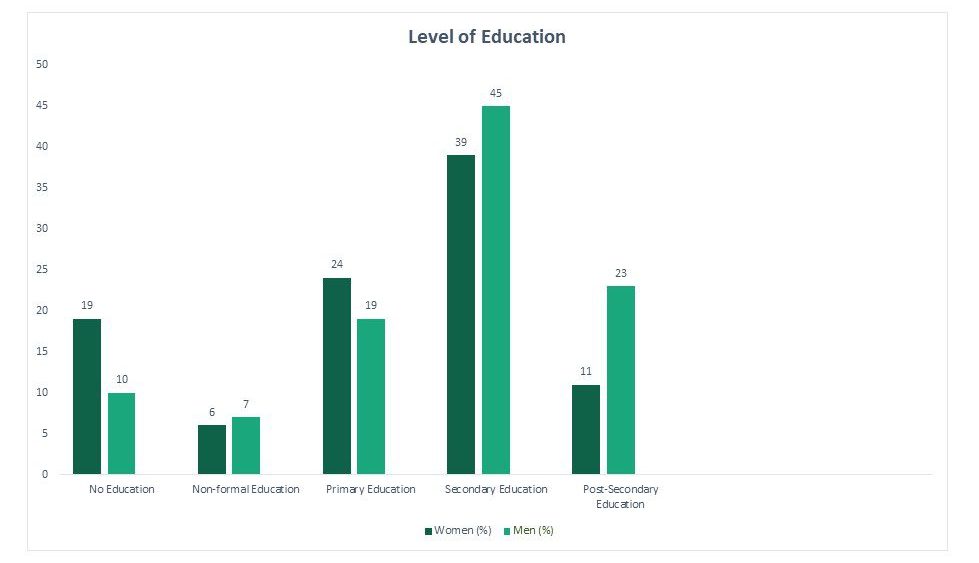

1. Level of Education

The completion rate of girls’ secondary education drops to 9% from 14% primary school completion. This means that the higher the level of education, the lesser the attainment for girls. Many girls are relegated to informal ambitions or no ambitions at all. In other words, this unequal access to education means that many women cannot compete favourably with men on income and that women are more likely to be unemployed, informally employed or take up lower-paying jobs than men. With education comes enlightenment, which will help the financial inclusion course. Gender inequality, especially in education, accounts for a dip in financial inclusion and a dip in economic development in Nigeria wholistically. Without levelling the playing field for both genders, specifically in education, achieving the NFIS may not be achieved by 2030.

Source: EFINA, pcl. research

2. Level of Income

Logically, the level of education directly correlates with the level of income. This means that where the level of education is low, the income level will correspond. These statistics and narratives are important because the basis of financial inclusion is education (mostly formal education); hence, this background disenfranchises women significantly.

Source: EFINA, pcl. research

This narrative also does not help the financial inclusion course. So, the closer we are to achieving gender equality, the closer we will be to achieving financial inclusion in Nigeria.

3. Deep-Seated Cultural Barriers and Social norms

Nigeria is highly driven by culture and religion, and gender inequality is often elevated on these platforms. Thus, any conversation about financial inclusion that doesn’t engage the torchbearers of culture and religion will be counterproductive. Cultural barriers that force early marriage on women contribute to this gender gap in financial inclusion. Early marriage, including childbearing, often limits educational attainment and self-development for women, which further impedes their income level. This implies that their access to credit/formal loans, insurance and savings is severely hindered. Furthermore, for cultural reasons, women’s education is still not prioritised in many Nigerian households compared to boys, so girls’ education is the most affected when there’s an economic setback or a global health crisis like the COVID-19 pandemic. EFINA rightfully states that socio-cultural norms and poverty are key factors in the gender gap in education.

Trust in FSPs

Source: EFINA, pcl. research

Women’s Financial Inclusion in Nigeria

In 2018, the Central Bank of Nigeria (CBN) constituted a subcommittee from the National Financial Inclusion Special Intervention Working Group to develop a framework to advance women’s financial inclusion in Nigeria. This framework proposed eight strategic points;

- Measures to support account opening

- Financial & digital literacy

- Deliver channels to serve women

- Systems of gender-disaggregated data collection

- Enabling environment required to achieve the government’s financial inclusion agenda

- Financially sustainable products and delivery systems

- DFS and fintech solutions

- Women leadership and staffing

Although the report on the framework recognises the deep-seated cultural barriers, social norms, low levels of education and income of women etc., the strategies do not directly engage the underlying problem of women’s financial exclusion. Financial inclusion is inherently an economic strategy, but where women are limited by cultural and social norms such as early marriages that inhibit independence and financial capacity, there is a need for a dedicated strategy that directly engages this.

The objective of this framework is two-phased; to reduce the gender gap in financial services from 8.5% in 2018 to half (4.2%) by the end of 2021and eliminate the gap by 2024. While there has been no published monitoring and evaluation on implementing the first phase of this framework, it can be inferred that this objective has not been met based on the general economic setbacks triggered by the Covid-19 pandemic.

How Nigeria can Close the Financial Inclusion Gender Gap

Closing the gender gap, not just for financial inclusion but also for economic advancement, is a joint effort of different stakeholders. As it pertains to financial inclusion, these stakeholders include the government, financial institutions, civil societies, NGOs, and cultural leaders (including religious leaders). Financial institutions have a social responsibility to close this gap, as they can serve as both a catalyst and a barometer for gender equality.

The following includes some recommendations for closing this gap:

- Public Policy: gender inequality is very much a policy issue that must be paid attention to by any serious government. It is important for the government to develop policies that encourage women’s financial inclusion, such as prioritising financial literacy for women in rural and urban areas and providing the infrastructure for institutions addressing this issue to thrive. Government regulations should enable ease of access to financial products and flexibility for the service provider. The government should also invest in awareness campaigns that shed light on the traditional issues that limit women’s inclusion.

- Incorporating Cultural Leaders as Strategic Components: cultural leaders need to be brought to the table for this conversation. While it may be a difficult conversation to have because of certain customary traditions, it is possible. For example, in an average Christian Nigerian family, the issue of investing in educating their female child to her desired level of education instead of marrying her off young would be given more thought if it came from their pastor or priest than from the child in question. It will also be more productive to have an Imam speak on the importance of having a bank account, the use of credit insurance or agent banking in his mosque than for a regular banker to do so. Cultural leaders are huge influencers among their followers, and this can be used to achieve the financial inclusion agenda.

- Incentivising Underserved Communities and Households: First, financial institutions must strengthen their grassroots and community engagement. This engagement includes collaborations with female-centred NGOs and other organisations that can provide incentives for women, especially those in rural areas, to use financial products. For example, a bank or insurance company can decide to sponsor free medical screening for women in these areas on the note that they open accounts with them. This can further be incorporated into the institution’s Corporate Social Responsibility (CSR).

- Leveraging Fintech: Fintechs in Nigeria have the potential to penetrate financial spaces that traditional financial institutions haven’t penetrated. In most cases, they are more affordable than traditional financial institutions. A good example is Kuda Bank which has zero charges on its debit card and zero debit fee, unlike other financial institutions. This affordability of fintech positions them as a more viable option for women with low income. Thus, if fintechs can focus on building women-centric financial products, the gender gap in financial inclusion will be reduced.

Summarily, It is not inclusion if financial services providers only cater to the minority of women in the formal sector.

Written by:

Henrietta Ifyede

Senior Analyst

![]()