Nigeria’s aviation sector is typically framed around visible symptoms: rising fares, fragile airline economics, and sub‑optimal infrastructure. However, these outcomes are manifestations of deeper systemic forces. As outlined in recent industry analysis, the sector is fundamentally being reshaped by foreign exchange (FX) volatility and Jet A1 fuel dynamics, which collectively define cost structures, pricing behaviour, and capacity decisions.

Between 2019 and 2025, Nigeria’s aviation industry has exhibited a persistent pattern: demand has remained structurally strong, yet access has continued to weaken. This contradiction reflects a market operating under macroeconomic constraint rather than sectoral inefficiency. This is not an industry crisis. It is a macroeconomic event playing out through aviation.

1. Demand Strength and Access Constraints in Nigerian Aviation

Nigeria’s aviation demand fundamentals are inherently strong. With a population exceeding 200 million, rapid urbanisation, and limited viable rail alternatives for intercity travel, air transport serves as a critical enabler of economic mobility, business connectivity, and regional integration. These structural factors position the country as a natural high-growth aviation market within Africa.

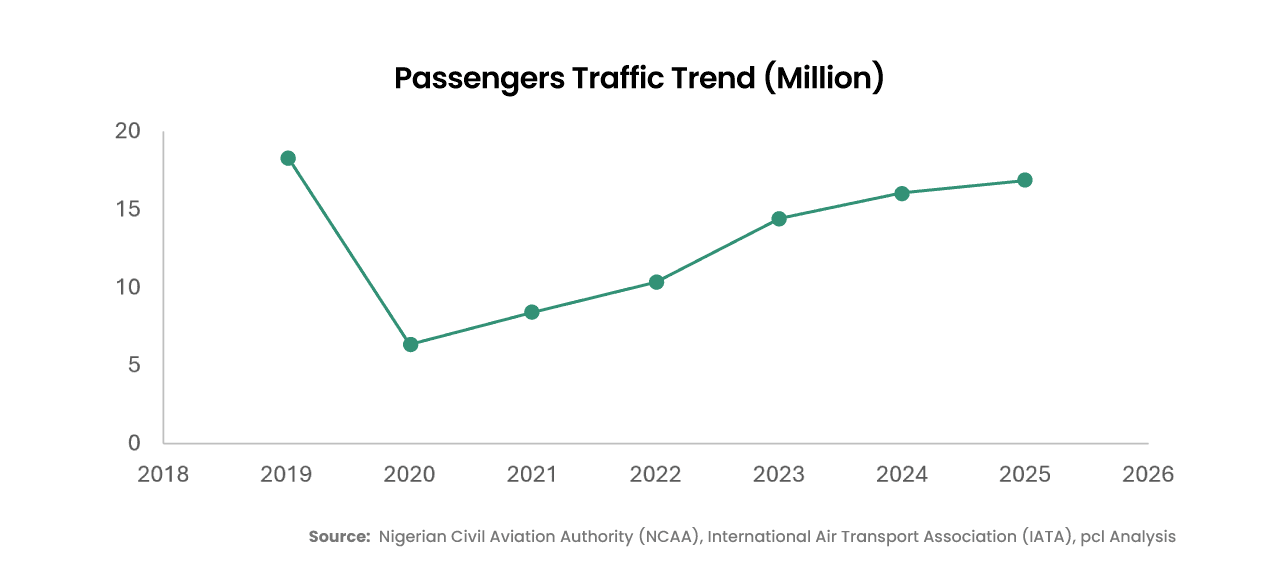

However, actual traffic performance reveals a persistent disconnect between latent demand and realised access. According to the Nigerian Civil Aviation Authority (NCAA), total passenger traffic reached approximately 18.1 million in 2019, comprising about 12.8 million domestic passengers and 4.4 million international passengers. By 2024, total traffic had declined to roughly 15.7 million, signalling only a partial recovery from pandemic-induced disruptions.

This underperformance becomes more pronounced when disaggregated. Domestic passenger volumes, which should reflect the depth of Nigeria’s internal mobility needs, stood at approximately 12.5 million in 2024, slightly below pre-pandemic levels. International traffic, at around 4.4 million passengers, has remained largely flat over the same period. Together, these trends point not merely to slow recovery, but to structural stagnation in segments of the market.

In effect, while Nigeria possesses the demographic and economic fundamentals to sustain significantly higher passenger volumes, actual traffic outcomes continue to fall short. This divergence underscores a critical reality: the constraint facing Nigerian aviation is not insufficient demand, but limited accessibility shaped by systemic economic and operational factors.

Airfares, particularly on international routes, have risen significantly in recent years, further widening the gap between demand and accessibility. According to the International Air Transport Association (IATA) and industry fare tracking data from platforms such as OAG, average ticket prices on major long-haul routes have increased substantially since 2019. While domestic passenger volumes have remained relatively flat at around 12 million since their pre-pandemic peak, international traffic has hovered near 4 million, according to the Nigerian Civil Aviation Authority (NCAA), well below the levels implied by Nigeria’s economic scale and regional importance.

This divergence is particularly evident on key international corridors. According to IATA and airline pricing disclosures, fares on routes such as Lagos–London have shifted from approximately $700–$900 in 2019 to $1,500–$2,500 by 2024–2025. When adjusted for exchange rate depreciation, using data from the Central Bank of Nigeria (CBN) and the World Bank, the effective cost to Nigerian travellers has increased even more sharply in local currency terms.

In practical terms, the Nigerian aviation market now functions as a “high-cost, low-access” system, one in which substantial latent demand exists, but elevated pricing and macroeconomic volatility constrain its full realisation, as also highlighted in recent industry analysis

FX and Fuel (Jet A1) Transmission Mechanism

At its core, Nigeria’s aviation sector operates under a structural imbalance: its cost base is largely dollar-denominated, while a significant share of its revenues is earned in naira. Aircraft leases, maintenance, insurance, and many international service charges are priced in U.S. dollars, whereas domestic ticket sales and a portion of outbound fares are realised in local currency. This exposes airlines to substantial exchange rate risk. According to the International Air Transport Association (IATA), such currency mismatches are a defining feature of airline economics in emerging markets.

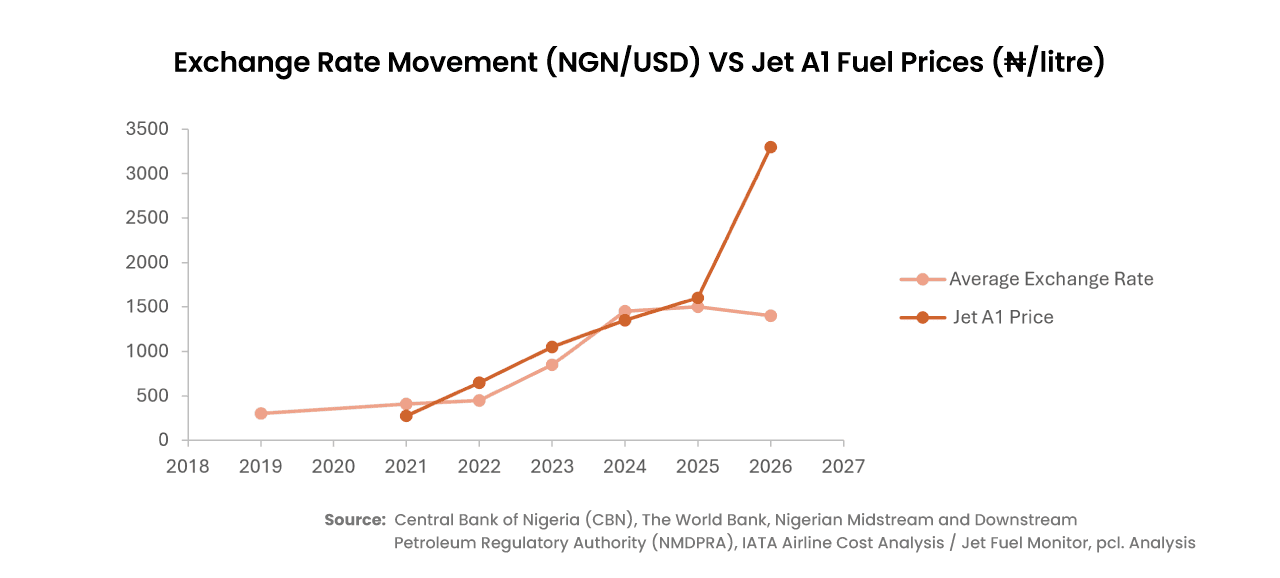

The foreign exchange environment in Nigeria has shifted dramatically. According to the World Bank’s World Development Indicators and Nigeria Macro Poverty Outlook reports, the naira depreciated significantly between 2019 and 2025 following FX liberalisation and macroeconomic adjustments. Accordingly, the NGN/USD exchange rate has moved from approximately ₦305 in 2019 to a range of ₦1,300–₦1,600 by 2025, with monthly averages exceeding ₦1,500 per dollar in several periods. This depreciation has directly inflated the naira-equivalent cost of dollar-linked inputs, forcing airlines either to increase fares or absorb significant margin compression.

Fuel dynamics further intensify this imbalance. Jet A1 aviation fuel, typically accounting for 30–45% of airline operating costs globally, according to IATA, has become the most volatile cost component in Nigeria’s aviation sector. Historically, Jet A1 prices rose from approximately ₦250–₦300 per litre in 2021 to about ₦1,200–₦1,300 per litre by mid-2025. However, recent geopolitical developments have significantly worsened the situation.

Following the escalation of the Iran-related conflict and disruptions to global oil supply routes, Jet A1 prices in Nigeria surged sharply in early 2026. According to industry reports and regulatory disclosures, prices increased from around ₦900 per litre in late February 2026 to between ₦3,000 and ₦3,300 per litre by April 2026, representing a rise of over 300% within weeks. In response, the Nigerian Midstream and Downstream Petroleum Regulatory Authority (NMDPRA) introduced price benchmarks ranging from approximately ₦1,760 to ₦2,800 per litre, while warning that volatility linked to the Iran conflict could persist.

Globally, the impact has been equally pronounced. According to recent reports, jet fuel prices have increased by 70–84% since the onset of the conflict, significantly raising airline operating costs worldwide.

The interaction between FX depreciation and fuel inflation creates a compounding cost effect. As the naira weakens, the cost of importing fuel rises in local currency terms, further amplifying operating expenses. Airlines respond by raising fares, which suppresses demand and reduces load factors. Lower load factors, in turn, raise unit costs, reinforcing upward pressure on pricing.

In Nigeria, airlines are not merely reacting to current cost conditions; they are pricing in anticipated volatility. This results in the incorporation of risk premiums into ticket pricing, reflecting uncertainty around FX availability, fuel supply disruptions, and broader macroeconomic instability.

The Cost of Instability: Blocked Funds and Risk Premiums

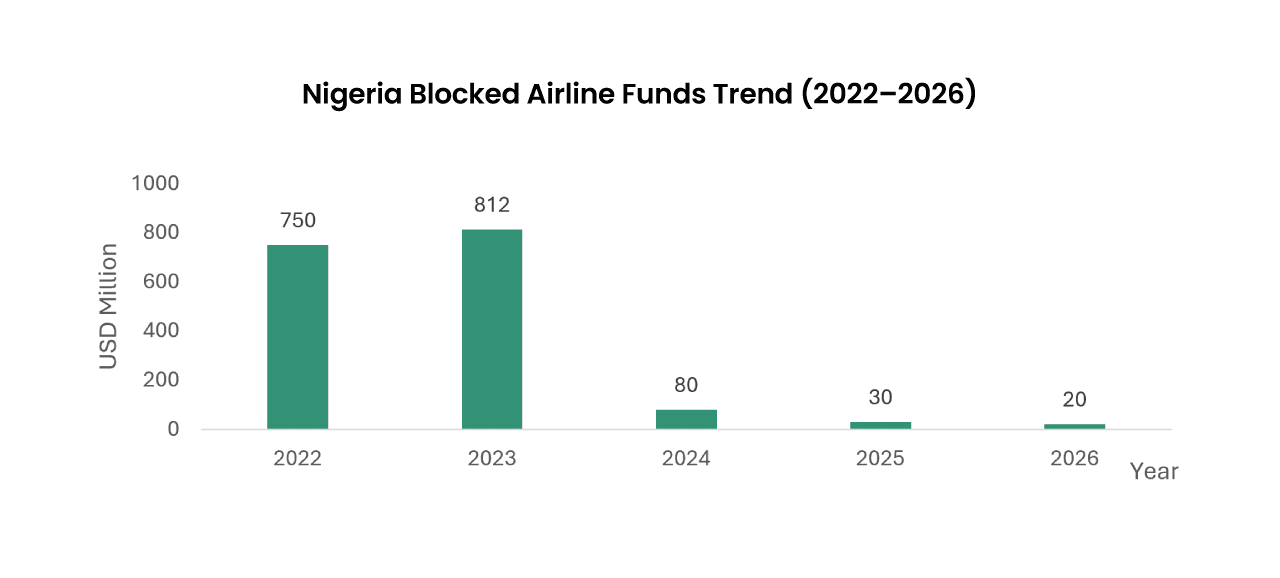

This macroeconomic environment crystallised most visibly in Nigeria’s blocked funds crisis, which became a defining moment for the aviation sector. Nigeria ranked first on the global list of unrepatriated airline revenues and became the single largest country globally for blocked airline funds. According to the International Air Transport Association (IATA), approximately $812 million in airline funds were trapped within the country during this period, accounting for about 35–36% of total blocked airline funds globally. The primary driver was a severe shortage of foreign exchange, which constrained local banks’ ability to meet repatriation requests, even as airlines continued to generate revenue from passenger and cargo operations.

By mid-2024, significant progress had been made. According to IATA updates, roughly 98% of these blocked funds had been cleared, reflecting targeted interventions and improvements in FX liquidity by the Central Bank of Nigeria CBN). By 2025, residual balances had reduced to minimal levels. As of 2026, the issue has transitioned from a systemic constraint to a largely resolved risk, although occasional FX access delays persist. While this marked an important step toward restoring confidence, the episode left a lasting structural impact on the market.

The crisis fundamentally altered how international airlines perceive and price risk in Nigeria. The experience of trapped revenues increased the perceived cost of doing business in the country and reinforced more conservative operational strategies. Several carriers reduced frequencies, delayed expansion plans, or temporarily suspended services during the peak of the crisis.

In this context, pricing behaviour has evolved beyond simple cost recovery. Airlines operating in Nigeria now adopt risk-adjusted pricing frameworks, where fares reflect not only underlying demand and operating costs, but also the probability and financial impact of macroeconomic disruptions. Route decisions are increasingly influenced by exposure to FX constraints, potential liquidity bottlenecks, fuel supply volatility, and broader currency instability.

This shift has had subtle but far-reaching implications. As risk premiums become embedded in ticket prices, the market is effectively re-priced, not just in monetary terms but also in terms of accessibility. The outcome is a system in which fewer passengers can afford to travel, and airlines operate fewer routes than the market would otherwise sustain. In effect, macroeconomic instability has quietly reshaped both who can fly and how Nigeria connects to the global aviation network.

From Volume to Survival Economics

Under stable macroeconomic conditions, aviation operates as a volume-intensive industry, optimised around connectivity, high load factors, and network density. Profitability is typically driven by scale, moving more passengers across increasingly efficient route networks. In Nigeria’s current environment, however, this model has been fundamentally disrupted. The sector is increasingly functioning as a yield-optimised, survival-oriented market, where airlines prioritise financial resilience over expansion.

As a result, airline strategies have shifted in three key ways:

- A focus on revenue per passenger rather than total throughput

- Prioritisation of high-yield corridors over broad network coverage

- Emphasis on short-term liquidity preservation over long-term capacity expansion

This structural shift has produced several far-reaching consequences.

First, demand has become increasingly segmented. As fares rise, driven by FX volatility and fuel cost pressures, price-sensitive segments such as SMEs, middle-income households, and leisure travellers are progressively priced out of the market. In contrast, corporate, government, and high-net-worth passengers remain relatively insulated. This has led to a narrowing of the demand base and a reduction in market resilience. Domestic passenger volumes, for instance, have declined by roughly 10% in recent years, while international traffic remains volatile and below potential (Federal Airports Authority of Nigeria, FAAN).

Second, airline behaviour has become more defensive. Faced with persistent cost pressures and macroeconomic uncertainty, carriers are reducing flight frequencies, selectively deploying capacity, and delaying expansion plans. This cautious approach persists even as passenger volumes show partial recovery. The implication is significant: Nigeria’s ability to function as a regional aviation hub is constrained, not by lack of demand, but by the inability of airlines to operate at scale under current conditions.

Third, Nigeria’s regional competitive position has weakened. Traffic that would naturally transit through major hubs such as Lagos or Abuja is increasingly being diverted to more stable aviation centers. Airports such as Kotoka International Airport and the Addis Ababa hub benefit from more predictable operating environments, enabling airlines to price more competitively and maintain broader network coverage. As a result, Nigeria is not experiencing a loss of demand per se, but rather a diversion of connectivity, with passengers and routes shifting toward markets with lower operational risk.

Why Other African Hubs Are Outperforming

Nigeria’s relative underperformance becomes clearer when benchmarked against leading African hubs such as Addis Ababa Bole International Airport and Kotoka International Airport. Despite facing similar global cost pressures, these markets outperform Nigeria due to stronger system-level efficiency and their ability to convert demand into scalable, predictable connectivity.

1. FX Regime as an Enabler of Capacity

In higher-performing hubs, foreign exchange policy functions as enabling infrastructure. Ethiopia’s prioritised FX framework reduces uncertainty around revenue repatriation and dollar obligations, compressing risk premiums and encouraging the deployment of airline capacity.

Nigeria, by contrast, remains constrained by FX unpredictability. Even after the resolution of blocked funds, persistent uncertainty continues to elevate pricing and suppress capacity through embedded risk premiums.

2. Fuel Economics and Volatility Management

While jet fuel is globally priced, local delivery systems determine real operating conditions. Competing hubs benefit from more efficient supply chains, stronger logistics, and greater storage capacity, thereby reducing volatility at the point of use.

Nigeria’s fuel ecosystem amplifies global shocks through supply inefficiencies and infrastructure gaps, turning fuel into a binding constraint on fares, route viability, and frequency.

3. Hub Architecture and Network Coordination

The most decisive difference lies in network design. Ethiopia’s hub model, anchored by Ethiopian Airlines, aggregates demand through coordinated scheduling, dense connectivity, and integrated long-haul and regional flows.

Nigeria’s fragmented multi-carrier structure lacks a central network orchestrator, limiting its ability to achieve scale, connectivity, and transfer traffic. As a result, strong origin demand is not translated into hub-level competitiveness.

A System Efficiency Gap

Nigeria’s challenge is not demand, geography, or market size; it is a system conversion efficiency.

Leading hubs operate as integrated systems where:

- FX policy reduces financial friction

- Fuel ecosystems dampen volatility

- Network structures maximise connectivity

Nigeria, in contrast, remains a demand-rich but system-constrained market, where these same factors limit scale and accessibility. Until the aviation system becomes more coordinated and macro conditions are more stable, demand will continue to be diverted, and Nigeria’s hub potential will remain under-realised.

A Sector at an Inflexion Point

As of April 2026, Nigeria’s aviation sector is in a transitional phase marked by partial recovery but persistent structural fragility. Improvements in FX liquidity and the clearance of most blocked airline funds have restored some confidence, yet access to foreign exchange remains inconsistent, and Jet A1 fuel prices continue to exert significant cost pressure.

This creates a “fragile recovery” environment:

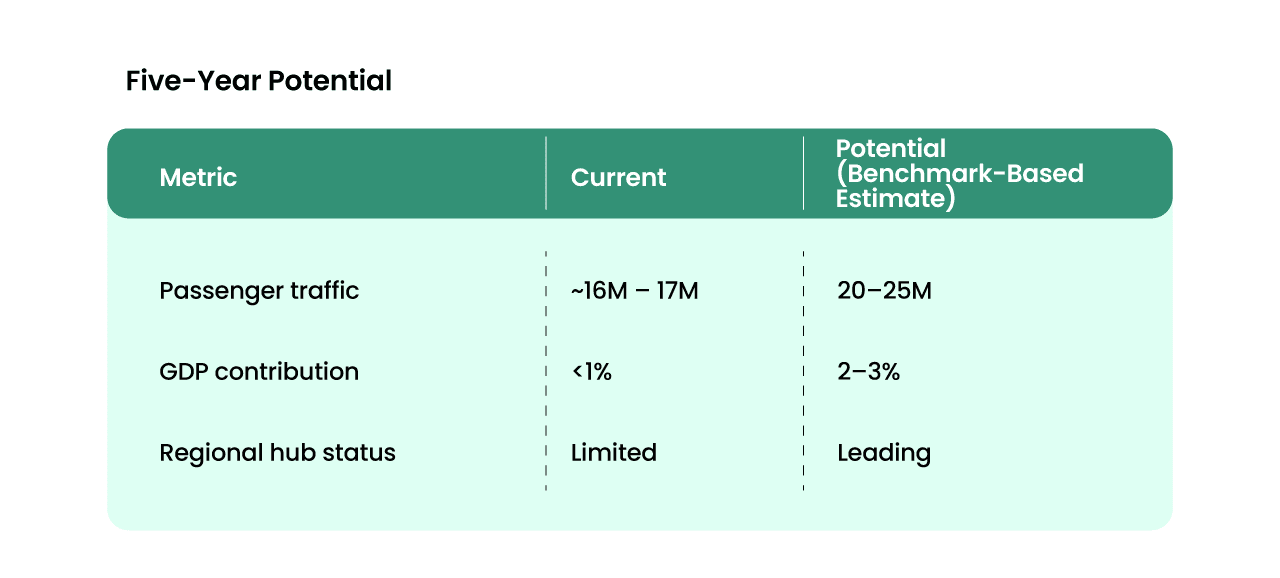

- Passenger traffic is recovering, reaching approximately 16–17 million, but remains below its market potential of 20-25 million. This reflects underlying constraints rather than weak demand.

- Airlines are cautiously optimistic, but still hedging against volatility, as fuel prices remain materially higher than pre‑2023 levels.

- The system is more stable than in 2023, but still far from being attractive for large‑scale, long‑term investment.

Aviation performance in Nigeria is highly sensitive to macroeconomic conditions. While incremental improvements deliver limited gains, sustained stabilisation in FX and fuel dynamics could unlock significant growth, including expanded connectivity, lower fares, and stronger regional hub positioning.

The Aviation Reset Agenda

Unlocking Nigeria’s aviation potential requires coordinated action across three critical systems:

- Monetary and FX policy: Aviation must be repositioned from a purely commercial activity to a strategic infrastructure sector within Nigeria’s economic framework. As demonstrated during the blocked funds crisis, access to foreign exchange is not merely a financial variable; it is a determinant of market participation and capacity deployment. The priority is not just access to foreign exchange, but predictability and consistency, which are essential to reducing risk premiums and restoring airline confidence.

- Energy and fuel markets: Jet A1 fuel pricing represents the single most volatile and impactful cost driver in Nigeria’s aviation sector. While global oil prices set the baseline, domestic outcomes are heavily influenced by local supply-chain inefficiencies, regulatory constraints, and logistics bottlenecks. Jet A1 pricing must be addressed as a supply-chain and efficiency challenge, as elevated and volatile fuel costs remain a primary driver of high airfares.

- Transport and hub strategy: Nigeria’s aviation strategy must move beyond reactive policy and explicitly target regional hub positioning. Given its population size, geographic location, and economic weight, Nigeria is structurally positioned to dominate West African aviation. However, this potential remains underutilised.

Realising hub status requires coordinated investment across:

- Airport infrastructure and terminal efficiency

- Air traffic management systems

- Seamless integration between domestic and international networks

Nigeria must adopt a deliberate strategy to become a regional aviation hub, supported by investments in infrastructure, connectivity, and operational efficiency. Aviation performance in Nigeria is shaped less by airline operations and more by the alignment of macro-financial stability, fuel economics, and connectivity strategy.

Pathways for the Next Five Years

The trajectory of Nigeria’s aviation sector will depend on how FX stability, fuel dynamics, and policy coordination evolve. Three plausible scenarios illustrate the range of outcomes.

Scenario 1: Stabilisation and Unlocking (High Upside)

Sustained improvements in FX liquidity, combined with reduced volatility and more efficient Jet A1 supply chains, lower operating uncertainty. Risk premiums decline, enabling airlines to reduce fares and expand capacity.

- Passenger traffic rises toward 22–25 million

- Nigeria strengthens its position as a West African hub

- Connectivity improves across both regional and long-haul routes

Scenario 2: Partial Improvement (Base Case)

FX access improves intermittently, but volatility persists, while fuel costs remain elevated. Airlines maintain cautious expansion strategies and continue pricing in risk.

- Passenger traffic stabilises around 18–20 million

- Limited network expansion

- Nigeria remains a large but under-optimised market

Scenario 3: Persistent Instability (Downside Risk)

Renewed FX constraints or continued fuel shocks sustain high-cost pressures. Risk premiums remain elevated, and airlines further reduce exposure to the market.

- Passenger traffic stagnates or declines below 17 million

- Increased diversion of traffic to competing hubs

- Further erosion of Nigeria’s regional aviation relevance

Across all scenarios, one conclusion is consistent: Aviation outcomes in Nigeria are not demand-constrained; they are policy and macro-condition-dependent.

Conclusion

The future of Nigerian aviation will not be determined in airline boardrooms alone. It will be determined at the intersection of currency stability, fuel efficiency, and regional connectivity strategy.

If these forces remain misaligned, the sector will remain a high-cost, low-access market, suppressing middle-class mobility and weakening Nigeria’s role in African trade and integration. If they are aligned, Nigeria can transition from a constrained point‑to‑point market to a true regional hub, generating substantial economic spillovers and unlocking latent demand.

The crisis is hidden, but the solution is clear. Rewrite the macroeconomic conditions under which Nigerian aviation operates and let the market finally grow to its full potential.