In January 2026, Nigeria’s Federal Government announced the establishment of a $2 billion National Climate Change Fund, designed to finance emissions reduction, renewable energy expansion, and climate resilience across the country (Energy News Africa, 2026).

The Fund forms part of a broader national transition agenda anchored by Nigeria’s Energy Transition Plan (ETP), which aims to achieve net-zero emissions by 2060 while expanding access to affordable, reliable energy. The Plan estimates that approximately $500 billion in investment above business-as-usual spending will be required to deliver this ambition. Progress is already underway. The Energy Transition Office has mobilised more than $3.6 billion from international partners, signalling early momentum and demonstrating Nigeria’s ability to attract catalytic climate finance at scale (Sustainable Energy for All, 2025).

The scale of the transformation envisioned is substantial. According to Sustainable Energy for All (2025), the Energy Transition Plan targets emissions reductions across five core areas: power, cooking, transport, industry, and oil and gas. The plan projects total installed electricity capacity rising to 277 gigawatts, with renewable energy forming the backbone of future supply.

At the same time, the introduction of a Climate and Green Industrialisation Investment Playbook is intended to unlock between $25 billion and $30 billion annually in climate finance, positioning Nigeria to draw sustained private and institutional capital into the transition (TheCable, 2026).

Underlying these initiatives is the Climate Change Act 2021, which provides the legal and institutional backbone for Nigeria’s climate agenda. The Act establishes governance structures, financing mechanisms, and national carbon reduction frameworks, including oversight by the National Council on Climate Change.

Taken together, these developments signal a fundamental shift. Nigeria’s climate economy is not approaching. It is here. The question this article asks, and the question every Nigerian board and executive team should be asking right now, is whether their organisation is prepared to operate inside it.

The Scale of What Is Moving

Over 80 million Nigerians lack access to electricity; the World Bank estimates this figure at approximately 86.8 million, underscoring the depth of the access challenge (World Bank, 2025). The Energy Transition Plan, therefore, addresses both decarbonisation and development simultaneously. The economic case reinforces this positioning. The estimated $500 billion investment required for the transition is projected to generate $686 billion in fuel savings over time, indicating a net economic benefit rather than a cost.

The investment is already moving. The African Development Bank Group maintains 52 active projects in Nigeria with total commitments of $5.1 billion, reflecting sustained institutional confidence in the country’s transition trajectory (African Development Bank Group, 2025).

Additional financing is being deployed across sectors. World Bank programmes alone include large-scale investments in power, irrigation, health systems, and agriculture, including a $1.57 billion financing package and multiple $500 million interventions targeting climate resilience and productivity (World Bank, 2026). UK-supported FCDO programmes further reinforce this landscape, with multi-year climate and agricultural initiatives aimed at strengthening resilience and rural economic systems (UK FCDO, 2023).

International development capital is not waiting. It is actively seeking Nigerian institutions with the governance capacity, execution capability, and credibility to effectively absorb and deploy it. Yet capital alone does not create economic transformation. Institutions do.

The regulatory environment is hardening in parallel. Nigeria’s Financial Reporting Council has established a phased timeline for adoption of the International Sustainability Standards Board’s disclosure frameworks: IFRS S1, covering general sustainability-related disclosures, and IFRS S2, covering climate-related financial risks and opportunities. Mandatory compliance for all Public Interest Entities begins in 2028.

The Central Bank of Nigeria, the Securities and Exchange Commission, and the Nigerian Exchange Group have each introduced frameworks that elevate ESG from voluntary reporting to a core component of market integrity, creditworthiness, and risk management. For Nigerian organisations, this is not a distant regulatory obligation. It is a commercial condition that is already shaping how capital is allocated, how contracts are awarded, and how investment risk is assessed.

Where Nigerian Business Actually Stands

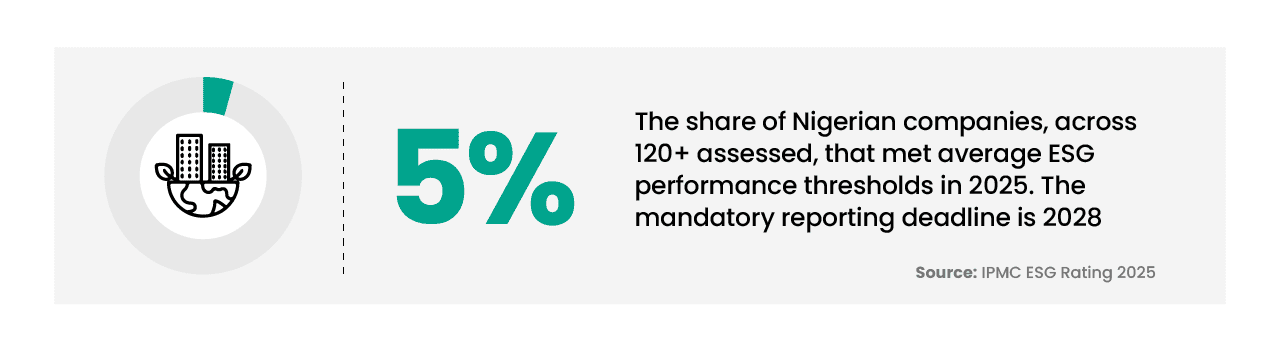

The gap between the scale of Nigeria’s climate economy and the readiness of Nigerian organisations to participate in it is significant and well-documented. The 2025 IPMC ESG Ratings Report assessed over 120 Nigerian companies across manufacturing, financial services, oil and gas, telecommunications, and professional services. Its findings were stark. Only 5% of assessed companies met average ESG performance thresholds.

Nigeria ranked third in Africa in ESG compliance, behind South Africa and Kenya, with an overall performance level of approximately 32%. Even in the financial services sector, Nigeria’s strongest ESG performer, only 12% of assessed institutions had disclosed financed emissions or climate-related credit exposures. Global data platforms such as the Carbon Data Project and Sustainalytics provide scant information on Nigerian companies, thereby directly limiting the flow of international capital into the country.

The barriers are structural. A 2025 assessment of Nigeria’s ESG landscape identified three recurring constraints across sectors: first, a shortage of trained sustainability professionals within firms, people who can manage GHG inventories, interpret IFRS S2 requirements, and design credible disclosure processes. Second, limited familiarity with international reporting frameworks, including GRI, SASB, TCFD, and the ISSB standards, and the practical difficulty of translating them into operational reality. Third, a cultural framing of ESG as philanthropy or reputational management rather than as financial risk and commercial positioning.

This last point deserves particular attention. ESG is not philanthropy. It is increasingly the mechanism by which capital is allocated, contracts are awarded, and creditworthiness is assessed. For Nigerian organisations seeking DFI co-financing, international supply chain partnerships, or access to green finance instruments, the absence of credible climate and sustainability positioning is no longer a gap to be addressed later. It is a liability being priced today.

The greatest climate risk facing many Nigerian organisations is not physical exposure to climate change. It is organisational unpreparedness for a market that is already changing around them.

This Is an Organisational Problem

What is missing in most Nigerian organisations is the internal infrastructure to respond to this landscape, organisational transformation and deliberate capability development, the same disciplines that define every serious change programme.

Climate readiness at the organisational level requires the following:

1. Strategic clarity. Board-level decision about how climate risk and opportunity intersect with the organisation’s core business model, with implications for investment priorities, operating model design, commercial relationships, and risk appetite.

2. People capability. Sustainability officers who understand GHG accounting. Finance teams who can work with IFRS S2. Operations leaders who can identify and reduce Scope 1 and 2 emissions. Procurement functions that can assess supply chain climate risk. These capabilities do not exist at scale in Nigerian organisations. They must be built, deliberately and systematically.

3. Process and data infrastructure. Climate performance must be measured, tracked, reported, and verified. This requires internal data systems, structured processes, and, in many contexts, third-party assurance. It is not an annual exercise. It is operational.

4. Governance. Board-level oversight of climate risk, integration of sustainability metrics into executive accountability, and transparent external reporting. The organisations already doing this, Access and Zenith Bank, are not doing so out of altruism. They are positioning for capital markets and commercial relationships that will increasingly require it.

What Readiness Actually Requires

For most Nigerian organisations, the starting point is a structured climate readiness assessment: a diagnostic that maps current position across strategy, capability, process, data, and governance, and identifies the most material gaps relative to the regulatory timeline and the commercial opportunities at stake.

Five questions anchor that assessment:

1. Does the organisation have a board-level climate strategy, or only a sustainability policy?

2. What is the current state of greenhouse gas emissions data, Scope 1, Scope 2, and material

Scope 3 categories?

3. What internal capability exists to prepare, substantiate, and defend IFRS S1 and S2 disclosures?

4. How is climate risk currently integrated into enterprise risk management and strategic planning?

5. What climate-related opportunities, in green finance, in international partnerships, in supply chain

positioning, is the organisation currently unable to pursue because of capability or credibility gaps?

The answers to these questions determine the sequencing of action. Some organisations will find that governance must come first. Others will find that data infrastructure is the critical bottleneck. Others still will discover that the skills gap is the rate-limiting factor, and that the most urgent investment is in building people.

What is not available as a strategic option for any organisation that intends to remain competitive in Nigeria’s evolving regulatory and commercial environment is to treat this as a problem for 2027.

Written by:

Kemi Phillips

Transformation Partner

| Take the first step

At pcl., our Transformation and Capability & Learning teams work with Nigerian organisations to build the internal capacity to respond to exactly these challenges, across strategy, people, process, and governance. Request a complimentary Climate Readiness Diagnostic session with our team: enquiry@phillipsconsulting.net |